Loading...

Loading...

By [Author] | April 17, 2026

On April 17, Venture Global LNG closed a $1.75 billion senior secured term loan at its Calcasieu Pass facility — using the proceeds to retire preferred equity interests held by Stonepeak Infrastructure Partners. On the surface, it reads like routine debt management. It isn't. This transaction is a live demonstration of how LNG project capital stacks are designed to evolve, and why the layer you sit in — as a lender, equity investor, or offtaker — determines your exposure when commercial ramp-up gets messy. Given Venture Global's ongoing disputes with Shell, BP, and Repsol over cargo delivery, "messy" is not a hypothetical here.

If you negotiate offtake agreements, arrange project finance, or advise buyers evaluating U.S. LNG supply, understanding the three-layer capital stack is no longer optional. Calcasieu Pass just gave the market a detailed case study. Here's how to read it.

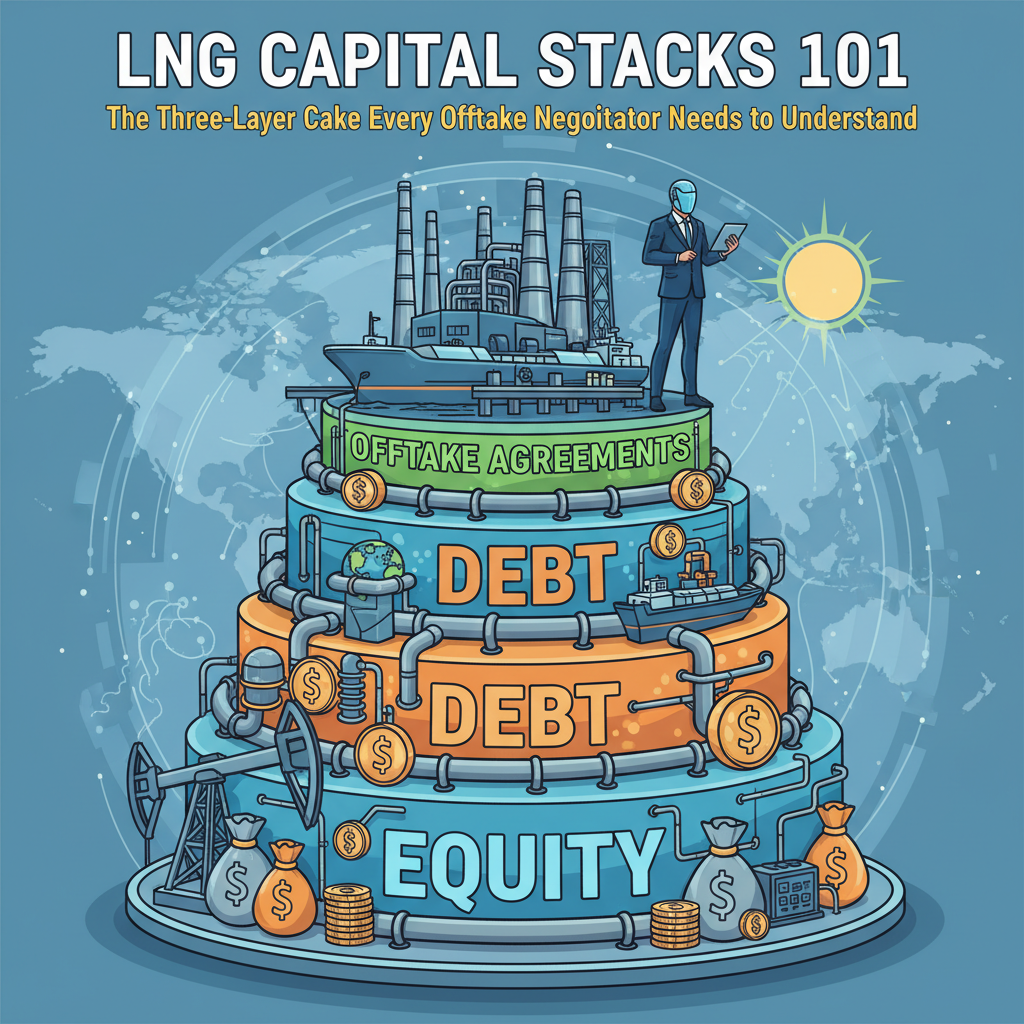

Layer One: Construction Equity — The Risk Capital That Gets the Shovel in the Ground

Every LNG project starts with a capital structure problem. Traditional project finance lenders — banks, institutional debt funds, export credit agencies — require demonstrated operational milestones before they will commit senior debt at scale. That means someone has to fund construction before the bankable milestones exist. That someone is the construction equity investor: the project sponsor, a private equity co-investor, or in some cases a strategic partner with upstream or offtake interests.

Construction equity sits at the bottom of the repayment waterfall. It absorbs cost overruns, schedule delays, and the full weight of commissioning risk. In exchange, it captures residual upside once all senior obligations are retired. For Venture Global at Calcasieu Pass, the sponsor itself carried substantial construction equity exposure — a structure that concentrated risk but preserved control over the project's development timeline and commercial decisions.

The critical implication for offtake negotiators: during the construction phase, the project's ability to meet cargo delivery commitments is entirely contingent on sponsor execution. There is no operational cash flow cushion, no debt service reserve funded by revenues, and no senior lender covenant package enforcing performance. Buyers signing long-term SPAs against construction-phase projects are, in effect, extending credit to the sponsor's balance sheet and project management capability.

Layer Two: Preferred Equity — The Bridge Instrument That Most Offtakers Never See

This is the layer the Calcasieu Pass refinancing put on the table. Stonepeak Infrastructure Partners held preferred equity interests injected during the construction phase — a structured instrument that sits above common equity in the waterfall but below senior debt. Preferred equity is not a loan. It carries no fixed maturity in the traditional sense, accrues a preferred return (typically targeting 12–18% IRR for infrastructure-focused funds), and is designed to be retired either through refinancing proceeds or project cash flows once operations stabilize.

Senior secured project finance term loans in LNG are currently clearing at approximately SOFR + 200–275 basis points for operational facilities with contracted cash flows — significantly cheaper than preferred equity returns targeting 12–18% IRR. The economics of retiring Stonepeak's position with term loan proceeds are substantial.

Why does preferred equity exist? Because when Calcasieu Pass was assembling its construction-phase capital stack, senior lenders were not yet prepared to commit at scale. Stonepeak filled the gap — providing capital that allowed construction to proceed while conventional project finance lenders waited for the milestones they required. This is a common bridge mechanism across mid-scale LNG projects, but it is expensive capital by design. The refinancing announced April 17 signals that Calcasieu Pass has now crossed the operational and cash-flow thresholds necessary to access investment-grade-adjacent term loan markets — retiring the expensive bridge and locking in cheaper permanent financing.

For offtakers, the preferred equity layer matters because it represents a senior claim on project cash flows ahead of any distribution to common equity holders — including the sponsor. If a project hits commercial ramp-up delays and cash flows compress, preferred equity holders can exert significant influence over project decisions before the sponsor sees a dollar of return. Understanding whether a project still carries preferred equity, and at what accrued return level, is a meaningful input into counterparty credit assessment.

Layer Three: Senior Secured Debt — The Layer That Defines Project Creditworthiness

The $1.75 billion term loan that replaces Stonepeak's preferred equity is now the senior secured layer at Calcasieu Pass. Senior debt sits at the top of the repayment waterfall, carries the strongest covenant protections, and is the instrument class that rating agencies, offtakers, and trade finance providers use as their primary reference point for project creditworthiness. The term loan is backstopped by Calcasieu Pass's DOE export authorizations — covering 12 MMtpa to FTA countries and approximately 9.98 MMtpa to non-FTA countries — and by the contracted offtake agreements that make those volumes bankable.[1]

The contrast with Exxon's Golden Pass situation is instructive. Reuters reported on April 17 that Exxon withdrew its offer to sell two initial Golden Pass LNG cargoes — a signal that cargo scheduling and offtake execution remain volatile even for projects with major-company backing.[5] Calcasieu Pass executed a successful capital stack refinancing on the same day, despite carrying unresolved offtake litigation with Shell, BP, and Repsol. The implication: term loan lenders have priced the litigation risk into their covenant package and concluded that contracted volume — even contested contracted volume — provides sufficient coverage. That is a meaningful signal about how the senior debt market is currently calibrating LNG commercial risk.

The parallel activity from NextDecade, which announced April 17 that it will deploy Honeywell liquefaction technology for its 30 MMtpa Rio Grande LNG terminal, suggests that mid-to-large developers are simultaneously locking in both technology stacks and capital stacks in Q2 2026.[2] A financing window appears to be open, and sponsors are moving to take advantage of it.

What to Watch Next

Three milestones deserve close attention in the next 12–18 months. First, watch Plaquemines LNG — Venture Global's sister project — for a similar preferred-to-term-loan conversion. If Plaquemines follows the Calcasieu Pass playbook, it will confirm that this capital stack evolution is a replicable template rather than a one-off transaction. Second, monitor FERC Docket CP16-454 for any amendments to Calcasieu Pass's operating authorization that could intersect with term loan covenant compliance. While this refinancing required no FERC approval — debt restructuring at operational LNG facilities does not trigger Section 3 Natural Gas Act review — any material change to the facility's authorization status would be relevant to lenders.[6] Third, watch whether the Venture Global offtake disputes with Shell, BP, and Repsol reach resolution or escalation; the outcome will test whether the term loan covenant package was structured conservatively enough to absorb a materially adverse commercial judgment.

The three-layer capital stack at Calcasieu Pass — construction equity absorbing development risk, preferred equity bridging the financing gap, senior debt providing permanent capital once milestones are met — is not unique to this project. It is the architecture that will define how the next wave of U.S. LNG facilities are built and financed. The Stonepeak exit gives the market a concrete data point on timing, pricing, and the operational thresholds that unlock each transition. Offtake negotiators who understand these mechanics will be better positioned to assess the creditworthiness of the projects they are evaluating — and to structure commercial terms that account for where a counterparty sits in that stack.

References

- "NextDecade to use Honeywell liquefaction technology for 30-MMtpy LNG terminal," Hydrocarbon Processing, April 17, 2026. https://hydrocarbonprocessing.com/...

- "NextDecade to use Honeywell liquefaction technology for 30-MMtpy LNG terminal," Hydrocarbon Processing, April 17, 2026. https://hydrocarbonprocessing.com/...

- "Italian small-scale LNG terminal gets 20th cargo," LNG Prime, April 17, 2026. https://lngprime.com/...

- "3 Utility Stocks To Grow Your Passive Income," 24/7 Wall St., April 17, 2026. https://247wallst.com/...

- "Exxon withdraws offer to sell two initial Golden Pass LNG cargoes, sources say," Reuters, April 17, 2026. https://reuters.com/...

- "FERC Demands $1.1 Billion in 'Large and Brazen Fraud Case'," RTO Insider, April 17, 2026. https://rtoinsider.com/...