Loading...

Loading...

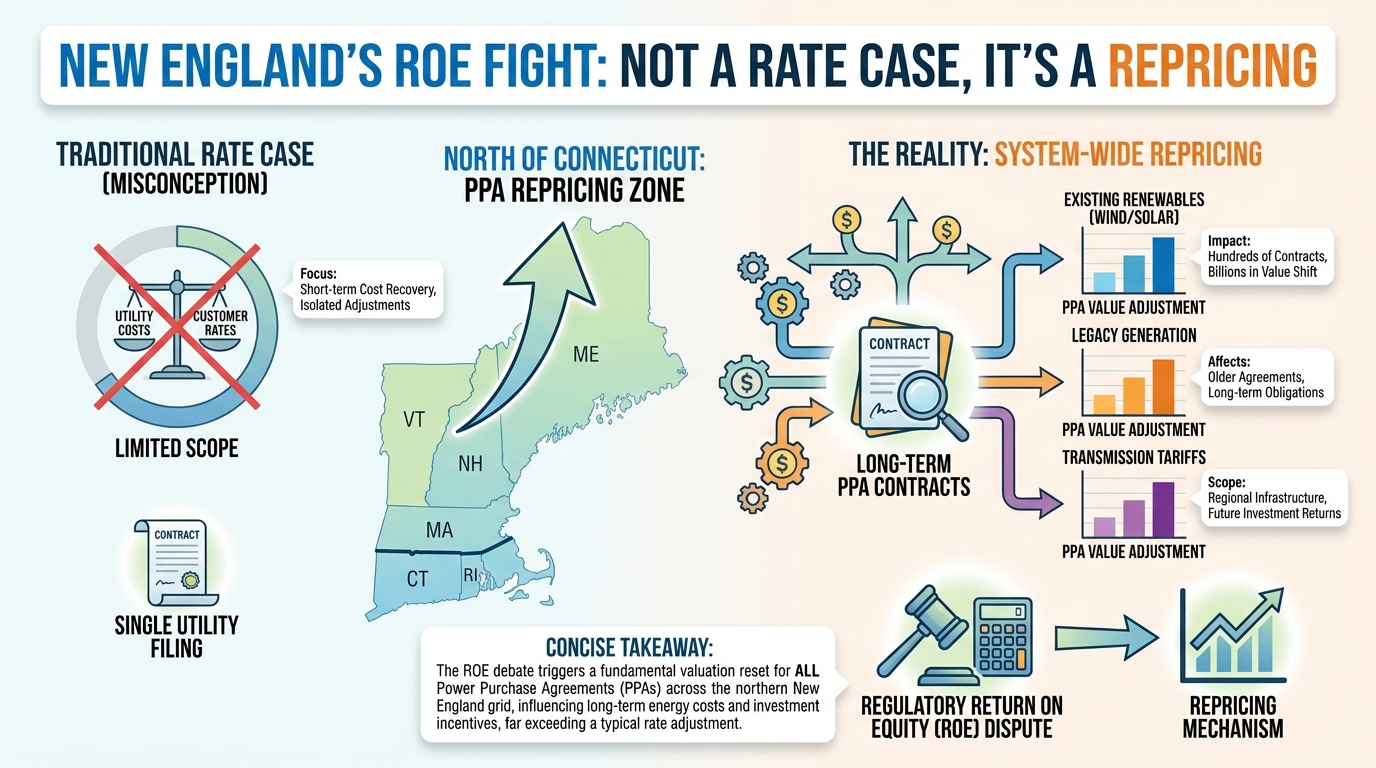

A month ago in these pages, I argued that ANEEL's Âmbar decision was not a consumer-protection ruling but a credit event — a regulator quietly repricing the bankable cashflows under Brazil's senior infrastructure debt. The mirror trade is now live in New England, and it points the other way. ISO-NE's transmission owners have asked the Federal Energy Regulatory Commission to raise their base return on equity, and the New England States Committee on Electricity (NESCOE), state attorneys general, and consumer advocates have lined up to oppose them.[1] Strip away the docket numbers and the substance is identical to the ANEEL fight: a regulator-versus-utility contest over the structural cost of capital sitting underneath every long-dated power contract in the region.

The same analytic frame, the opposite direction

In Brazil, ANEEL is pushing authorized returns and bankable cashflows down, forcing speculative developers out of the queue and re-rating senior infrastructure debt tighter. In New England, the transmission owners are trying to push their authorized base ROE up, and the states are fighting to keep it pinned. The direction of travel differs; the lesson for capital allocators does not. Authorized ROE — long treated by corporate offtakers and foreign infrastructure investors as a fixed input, a number you copy out of a FERC order into row 14 of a model — is a structural variable. It moves. And when it moves on a multi-billion-dollar regulated rate base, it moves the all-in delivered cost of every megawatt-hour contracted in that footprint.

That is why the ISO-NE proceeding is not, properly, a rate case. It is a repricing of the transmission cost layer embedded in every PPA, VPPA, and retail supply contract signed north of the Connecticut border.

Where the ROE actually shows up in a New England PPA

Corporate procurement teams typically decompose a New England PPA cost stack into four lines: the generator's contract strike, basis to the settlement node, capacity obligations, and "delivery" — the catch-all bucket where Regional Network Service (RNS), Localized Network Service, and assorted FERC-jurisdictional charges get parked. Delivery has historically been modeled as low-volatility pass-through noise. That assumption is what is breaking.

Base ROE is the multiplier on every dollar of transmission rate base. Apply a 50- to 100-basis-point shift to the New England TOs' combined net plant in service — already in the tens of billions, and set to expand sharply to accommodate offshore wind interconnections (Vineyard, Revolution, SouthCoast), HVDC interties to Québec and New Brunswick, and onshore reinforcement for electrification — and the arithmetic flows directly into the RNS rate. RNS is bundled into delivered energy cost. Delivered energy cost is what the corporate offtaker actually pays.

A higher authorized ROE on a growing rate base does not compound linearly. It compounds geometrically: the rate increases, and the base it is applied to is simultaneously expanding under the weight of the region's capex cycle.

This is the same compounding dynamic that made the Âmbar repricing matter in Brazil — small changes in the regulated return assumption, applied across a large and growing asset base, produce outsized swings in contracted cashflow value.

Two repricings, running simultaneously

What makes the New England event particularly acute is that the ROE proceeding is not happening in isolation. A parallel fight over who pays the transmission bill is unfolding across FERC's docket. Maryland's Office of People's Counsel has filed a Federal Power Act Section 206 complaint challenging PJM Schedule 12's socialization of regional transmission expansion costs; Oregon has approved a dedicated data-center rate class ring-fencing transmission riders to the load creating them; and FERC Commissioner Travis Kavulla's "segregated queue" framework would push interconnection-driven costs toward identifiable large loads rather than the historical socialized base.[2]

For an offtaker modeling a 15-year New England PPA, two independent variables are now in motion: the rate of return on the transmission rate base (the ISO-NE ROE fight), and the allocation of that rate base across load classes (the Maryland/Oregon/Kavulla axis). Either one alone is enough to invalidate a delivered-cost model. Together, they make "transmission as pass-through noise" an untenable underwriting assumption.

The affordability backdrop, and why the states are fighting hard

The political context matters because it shapes how FERC will receive the TOs' filing. At the 21 May New England regulators' symposium, state commissioners explicitly elevated grid infrastructure costs and supply-side pressures as their dominant 2026 concern.[3] The region is simultaneously absorbing the renegotiation of offshore wind contracts at materially higher strike prices, an interconnection queue that pv magazine reports is still logjammed on solar-plus-storage in most states,[4] and a capex wave for electrification reinforcement. Against that backdrop, NESCOE and the state advocates are arguing the TOs simply have not met the FPA Section 206 "just and reasonable" bar — that the capital-market evidence and peer-group methodology do not support a higher base return.[1]

This is the same affordability politics that is producing parallel battles on the generation side — Ohio's bill to let AEP and other regulated utilities own nuclear plants is the generation-side version of the same story, with consumer and industrial groups pushing back against expansion of rate-base eligible assets.[5] The throughline: regulated utilities are seeking to grow the size, scope, and return profile of their rate bases at exactly the moment state regulators have been told by their voters that affordability is the binding constraint.

What the advisory audience should actually do

For foreign infrastructure capital and corporate procurement teams with New England exposure, three practical implications follow.

First, unbundle the delivery line. The RNS component of a delivered-cost model should now be carried as a sensitivity, not a constant. A reasonable bracket — pending FERC's procedural posture — is a 50 to 100 bps base-ROE swing layered on a rate base projected to expand materially over the contract tenor. That is a meaningful $/MWh band on a 15-year PPA.

Second, model the allocation axis separately. If the Maryland 206 complaint or a Kavulla-style segregated queue framework is generalized to ISO-NE, large identifiable loads — hyperscaler campuses, electrified industrial sites — face a step-change in their share of transmission cost recovery, independent of what FERC does on ROE itself.

Third, read this as the Northern Hemisphere companion to ANEEL. Whether a regulator is pushing returns down (Brazil) or a utility coalition is trying to push them up against state resistance (New England), the message for sovereign and pension capital underwriting regulated transmission is the same: authorized returns are no longer a fixed input. They are the contested variable. The days of dropping a single ROE number into an IRR model and moving on are over.

The forward read

FERC's ruling on the ISO-NE TOs' request will not stay in New England. ROE complaints are already queued in MISO and PJM, and the methodological choices FERC makes here — on peer-group selection, risk-premium construction, and the treatment of incentive adders alongside the base — will travel. For offtakers, the practical horizon is the refund-effective date and any settlement-judge phase, which together set the window during which transmission cost assumptions in active PPA negotiations need to be re-marked. For the regulated transmission asset class as a whole, the proceeding is the clearest signal yet that the post-2026 PPA cost stack will be written in a different language than the one offtakers have been speaking for the past decade.

References

- "New England States, Advocates Denounce TOs' Request for Higher ROE," RTO Insider, 24 May 2026. Link

- "Transmission Cost Allocation" — institutional reference on PJM Schedule 12, Maryland OPC's FPA Section 206 complaint, Oregon's dedicated data-center rate class, and the Kavulla segregated-queue framework.

- "New England Regulators Grapple with Grid Infrastructure, Supply Costs," RTO Insider, 21 May 2026. Link

- "Most states face regulatory logjams on solar-plus-storage as interconnection procedures lag," pv magazine USA, 21 May 2026. Link

- "AEP, other Ohio utilities could own nuclear power plants under state bill," Utility Dive, 22 May 2026. Link

Leave a Comment